In the 12 months to the end of October, Australian Equities have returned 19.3% (as measured by the ASX 200 Total Return index) and International Equities have returned 15.8% (as measured by the MSCI World ex Australia Index). These exceptional returns, which include the market downturn that occurred this time last year, have brought welcome relief to investors after a poor 2018.

So how do we reconcile these returns with all the news about a less than rosy global economic outlook? The fact is, that these returns weren’t driven by improving company profits, rather they were driven by Central Banks, including our own Reserve Bank and the US Federal Reserve, continuing to either maintain a low interest rate environment or indeed to further cut interest rates.

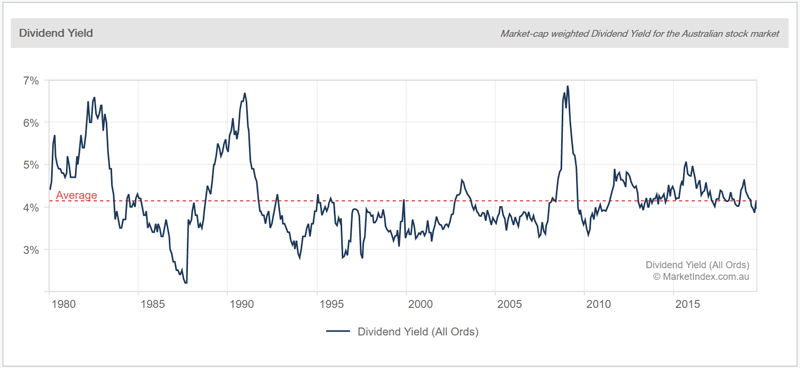

A low interest rate environment effectively supports increasing asset prices. This occurs because the low return on Cash encourages some investors to seek higher returns elsewhere. And it is this increased demand that fuels increasing asset prices. We measure this using the Price Earnings ratio. When share prices increase, without an underlying increase in earnings, you get an increase in the P/E ratio. As you can see from the chart below the P/E ratio for the ASX is now above the long-term average. This means there is some increased risk of a correction, but we are not yet near ‘bubble’ territory.

We therefore have some confidence that asset prices can continue to increase, particularly, if Central Banks cut interest rates further. There is an increasing probability that the RBA will cut the Cash Rate from 0.75% to 0.5%, early in the New Year. Just the fact that this is the consensus market viewpoint means that support for equities should be maintained.

Source: MarketIndex.com.au